Analysis of Maldives Tourism in May 2026: A Recovery Signal, Not Yet a Recovery Trend

04 Jun 2026, 19:09 · by i.zuhuree

May 2026 offered the Maldives a fragile recovery signal: arrivals improved, but the year remains behind target, occupancy is weak, and West Asia conflict continue to threatens air access. In this blog, I explain why tourism performance must be read carefully. The full May 2026 Monthly Brief goes deeper into the data, register your email to download the full brief for free.

In tourism, as in science, one data point can be a signal, a coincidence, or the beginning of a pattern. The difficult part is knowing which one we are looking at.

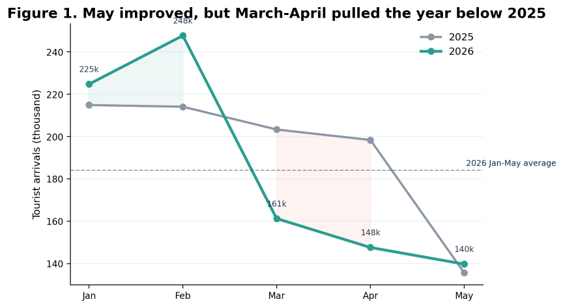

May 2026 gave the Maldives a small but important signal. Tourist arrivals reached 139,746, about 3% higher than May 2025. After a weak March and April, that improvement matters. It tells us that demand did not continue falling in a straight line. But it also tells us something more uncomfortable: the Maldives is still behind the pace of last year.

By the end of May, total tourist arrivals stood at 921,115. During the same period in 2025, the Maldives had received 966,358 visitors. That leaves 2026 about 4.7% behind last year’s run-rate. So the May result is not a full recovery. It is more like the first stable reading on an instrument after turbulence. Register to read full brief.

The annual target makes the challenge clearer. The Government has set a target of 2.5 million tourists for 2026. To reach it, the Maldives needs roughly 1.58 million additional visitors between June and December. That means an average of about 7,378 tourists per day for the rest of the year. May’s own daily average was about 4,508.

That gap is the real story. The Maldives does not simply need demand to stabilise. It needs the low season to perform unusually well, and then it needs a strong fourth quarter. That requires more than beautiful images, broad campaigns, or confidence that the brand will carry itself. It requires route-linked marketing, forward-booking intelligence, market-specific recovery plans, and careful protection of price discipline.

The harder truth is that arrivals are only the surface of the system. Under the surface are bed nights, occupancy, average stay, taxable spending, foreign exchange receipts, resort cash flow, guesthouse resilience, supplier payments, and government revenue. If arrivals improve but occupancy remains weak, the industry still feels stress.

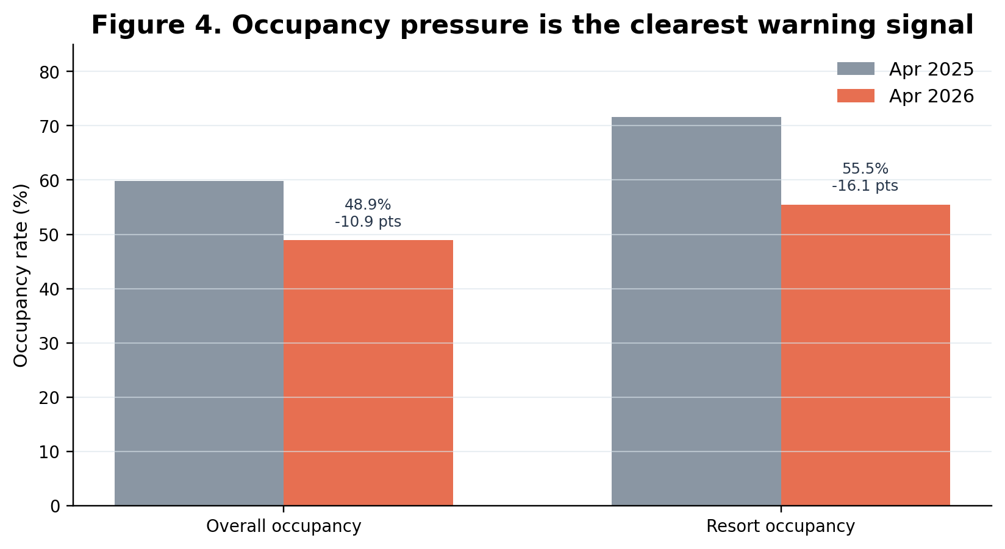

The latest detailed accommodation data available in the brief are for April. They show why the sector should be cautious. Overall occupancy in April 2026 was 48.9%, down from 59.8% in April 2025. Resort occupancy fell from 71.6% to 55.5%. Total bed nights declined from 1.14 million to just under 1.00 million.

This is where tourism becomes less like a headline and more like a living system. A resort bed is not just inventory. A guesthouse bed is not just capacity. Each bed is a claim on future demand. When the operational bed base reaches about 68,010 beds, and guesthouses account for roughly one quarter of that capacity, weak demand is no longer confined to large operators. It spreads across islands, workers, shops, transport providers, cafés, dive schools, farms, fish suppliers, and households.

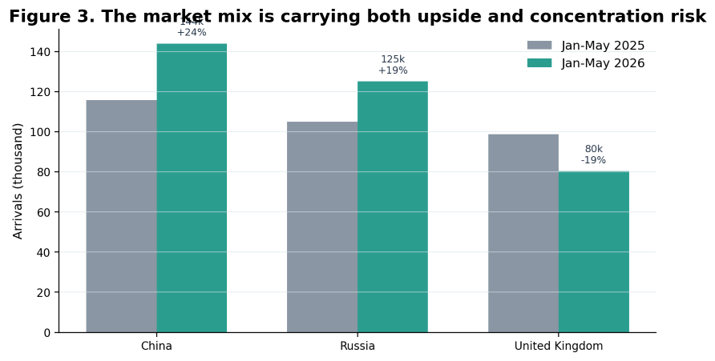

The source-market picture adds another layer. China remained the largest market by end-May 2026 with 143,917 arrivals. Russia followed with 125,096, and the United Kingdom recorded 80,323. Together, the top three markets accounted for about 38% of arrivals in the first five months.

That concentration can be useful when large markets perform. It can also become a vulnerability. China and Russia are ahead of their 2025 pace. The United Kingdom is materially weaker. The lesson is not that the Maldives should move away from its core markets. The lesson is that concentration must be managed like risk. A strong portfolio needs anchors, but it also needs shock absorbers.

This is where the war in West Asia enters the tourism story. The Maldives is geographically in the Indian Ocean, but commercially it is connected to the world through air corridors. Long-haul tourism does not arrive by magic. It moves through aircraft networks, hub airports, overflight permissions, fuel costs, airline confidence, insurance, traveller sentiment, and route economics.

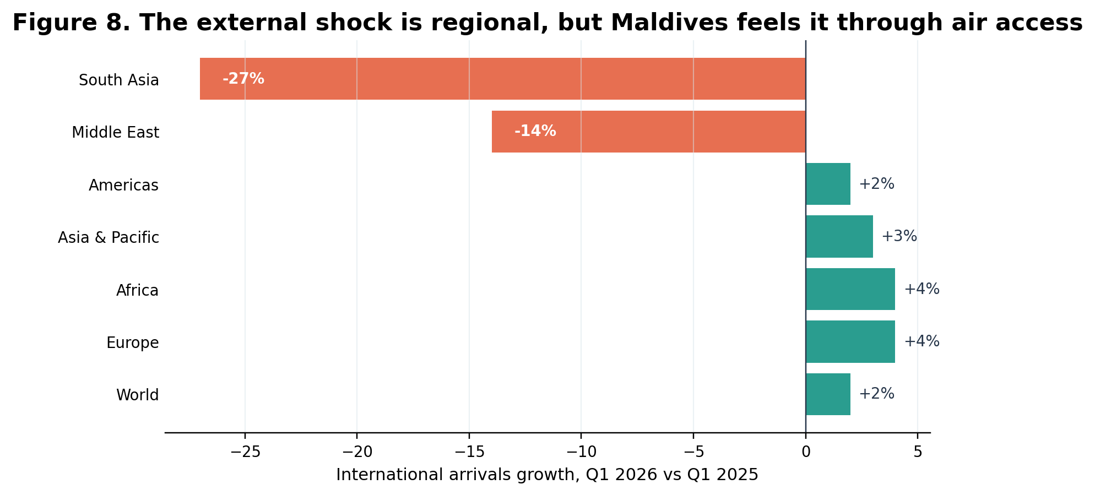

The May brief notes that global tourism was still resilient in early 2026, with UN Tourism reporting 2% growth in international arrivals in the first quarter. But the same global picture carries warning signs. The conflict in West Asia has weakened the outlook and is expected to reduce full-year international arrivals growth by 1–2 percentage points below the earlier forecast. The global data also show a 14% decline in Middle East arrivals and a 27% decline in South Asia in Q1, partly linked to disruption affecting Middle Eastern air hubs.

For the Maldives, this is not distant news. It is operational risk. Many travellers reach the Maldives through West Asian and Middle Eastern hubs. When that corridor becomes uncertain, the shock can move quickly into bookings, cancellations, airline schedules, transfer confidence, and travel insurance behaviour. In a destination where air access is the bridge between demand and revenue, geopolitical disruption becomes a tourism variable.

The fiscal channel is equally important. MIRA collected MVR 2.63 billion in April 2026. GST accounted for MVR 1.7 billion, or 63.6% of the total. Green Tax, Airport Development Fee, Departure Tax and resort rent are also tied to tourism activity. When arrivals, occupancy, bed nights or spending soften, the effect does not stay inside hotels. It reaches public revenue and foreign exchange liquidity.

The World Bank’s April 2026 macro outlook adds weight to this concern. It projects weak real GDP growth, with tourism revenue expected to fall amid fewer arrivals and shorter stays. It also projects inflation at 6.0% and a current-account deficit of 21.3% of GDP.

This is why tourism data must be read as macroeconomic intelligence. A weak occupancy number is not only an industry statistic. It is a signal about employment, imports, taxes, dollar flows, debt servicing, and public-sector space.

So what should be done now?

The first priority is air access security. The Maldives needs a practical tourism shock-response mechanism that links tourism, civil aviation, airports, immigration, central bank, tax authority and industry. The question is simple: are routes normalising, or should alternative routes, charters and market-specific support be activated?

The second priority is low-season conversion. Promotion should move from broad destination branding to route-linked campaigns that help people actually book. If travellers perceive uncertainty, operators need packages that reduce friction: room, transfer, meal plan, flexible booking and experience bundled clearly.

The third priority is yield protection. The temptation in a weak low season is discounting. But indiscriminate discounting can damage the very value the Maldives depends on. Tactical pricing, clear booking windows and value-adds are safer than a race to the bottom.

The fourth priority is market diversification. China, Russia and Europe must be protected, but secondary markets should be developed deliberately for shoulder-season travel. The Maldives needs demand that is not only large, but also balanced across seasons, routes and traveller motivations.

The full May 2026 Monthly Brief goes deeper into the data, including the demand dashboard, source-market portfolio, occupancy signals, external-risk exposure, fiscal implications and June–August watchlist.

Register your email to download the full brief for free and receive the next Maldives Tourism Observatory update when it is released.

The May signal is encouraging. But the scientific reading is careful: this is a recovery signal, not yet a recovery trend. The next test begins now.