The Maldives’ Seven-Night Tourism Reset: Why Fewer Nights per Visitor Could Reshape Tourism Strategy

27 May 2026, 10:18 · by i.zuhuree

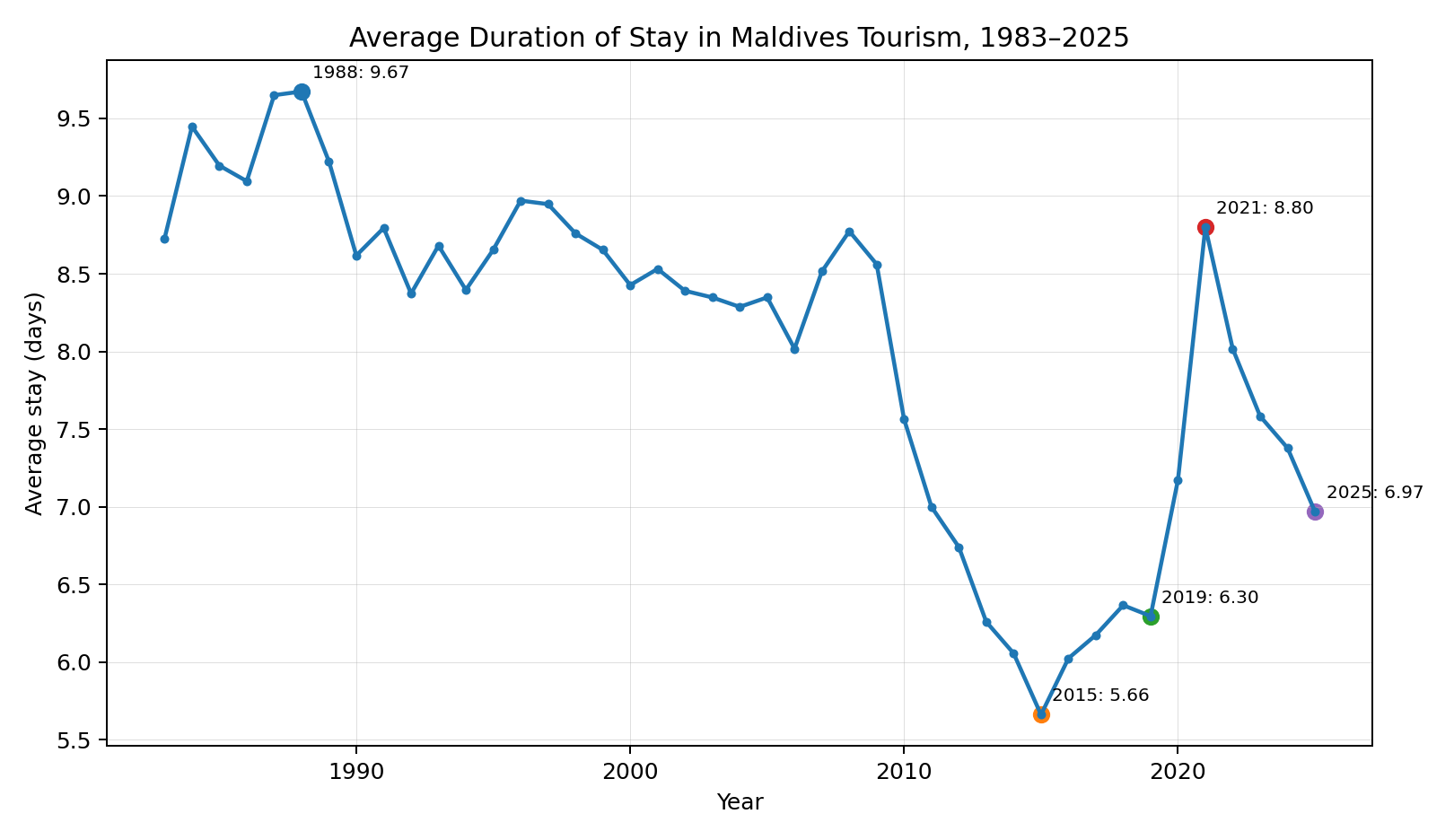

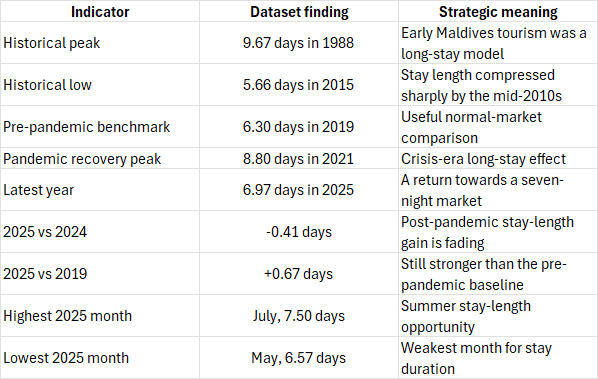

Is Maldives tourism quietly shifting from a long-stay destination to a shorter-stay, higher-turnover model? Average stay peaked at 9.67 days in 1988, fell to 5.66 in 2015, rebounded during the pandemic, and declined again to 6.97 days in 2025, down 5.5% from 2024. The issue is not arrivals alone; it is stay-adjusted value. Policymakers and operators should target segments, products, and packages that increase bed nights, yield, and destination value across the whole tourism economy over time.

When I analysed the latest average-duration-of-stay dataset for Maldives tourism, the most important story was not simply whether tourists are still coming. It was how long they are staying. For a destination like the Maldives, average stay is not a minor statistical detail. It affects room nights, occupancy, staffing, transfer demand, restaurant revenue, excursion sales, tax collections, waste generation, and the overall value captured from each visitor.

The dataset covers annual and monthly average duration of stay from 1983 to 2025, measured in days. It shows a long-term structural shift: Maldives tourism has moved from a high-stay model in the 1980s, when annual average stay was often above eight or nine days, to a shorter-stay model in the 2010s, when average stay fell close to six days. The pandemic temporarily reversed this pattern, pushing average stay up to 8.8 days in 2021. But by 2025, average stay had fallen to 6.97 days

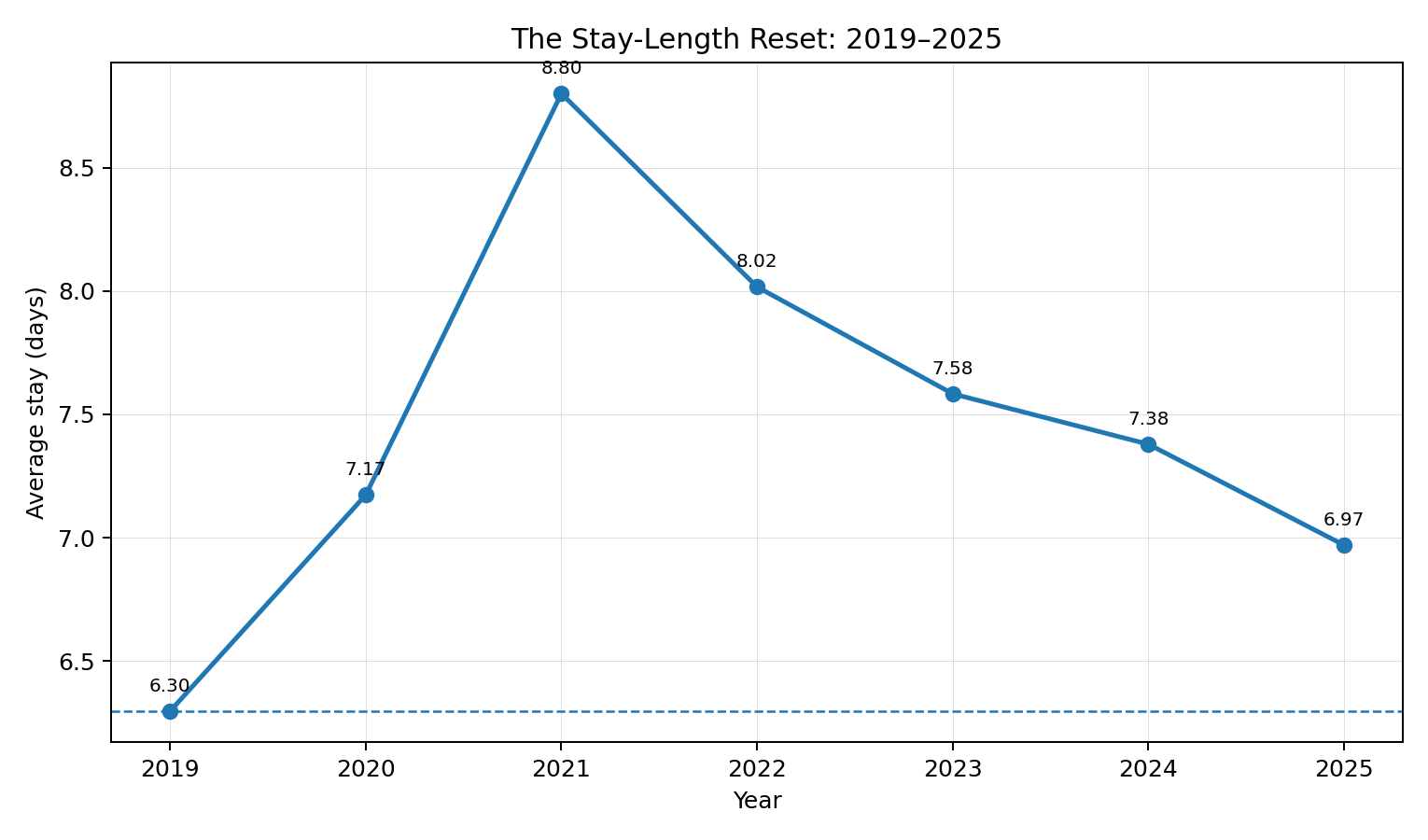

This is the key insight: the Maldives is moving out of the pandemic-era long-stay period and settling into a tighter seven-night tourism economy. That is not necessarily bad. The 2025 figure is still higher than the 6.30 days recorded in 2019. But it is a clear signal that the industry should not assume that the unusually long stays of 2021 and 2022 will continue. For policymakers, destination marketers, hotel operators, and investors, the practical question is now: how can the Maldives generate more value from a visitor who stays around one week?

Methodology and assumptions

I used the annual and monthly average-duration-of-stay values from the long-series source as Maldives Bureau of Statistics / Ministry of Tourism data for 1983–2024, with 2025 sourced from the Maldives Monetary Authority series 210 and treated as official provisional data. I use 2019 as the main pre-pandemic benchmark because it was the last full year before the COVID-19 disruption. I treat 2020 carefully because some monthly values, especially May and June, reflect crisis conditions rather than normal visitor behaviour.

The long-term decline in average stay

The first major pattern is the long-term shortening of tourist stays. The annual average stay peaked at 9.67 days in 1988. By 2015, it had fallen to 5.66 days, the lowest point in the dataset. This means the Maldives lost roughly four days of average stay between the late 1980s and the mid-2010s.

That long-term decline matters because it changes the economics of tourism. A destination can increase arrivals and still face pressure if visitors stay for fewer nights. Shorter stays mean each arrival produces fewer room nights, fewer meals, fewer excursions, and fewer opportunities for spending outside the room. For resorts and guesthouses, it also means higher operational turnover: more check-ins, more transfers, more cleaning cycles, and more marketing effort per occupied night.

The data suggests that the Maldives has already lived through a major transformation in visitor behaviour. The early tourism model was built around longer holidays. The later model became more compressed, more accessible, and more dependent on attracting higher visitor volumes to generate the same or greater number of bed nights.

The pandemic may have created a temporary long-stay effect

The second major pattern is the post-pandemic reset. In 2019, average stay was 6.30 days. In 2020, it increased to 7.17 days, but the year was distorted by travel restrictions and abnormal visitor movements. In 2021, average stay reached 8.8 days, the highest annual figure since the late 1980s.

This was not a normal market signal. It was a crisis-era pattern. The Maldives was one of the destinations that reopened relatively early, and global travel restrictions made trips harder to organise. Visitors who did travel often stayed longer. Some may also have combined leisure with remote work. The result was a temporary return to long-stay behaviour.

But the decline after 2021 is clear: By 2025, the long-stay effect had weakened significantly. Average stay declined by 0.41 days from 2024, or about 5.5%. This is not a small operational change. If a destination receives more than two million tourists, a reduction of 0.4 days represents a large number of lost visitor-days compared with the previous year’s stay pattern.

At the same time, I do not read 2025 as a return to weakness. The 2025 average stay of 6.97 days remains about 0.67 days higher than 2019. That means the Maldives has retained some post-pandemic stay-length gain, even though it has lost the exceptional long-stay pattern of 2021 and 2022.

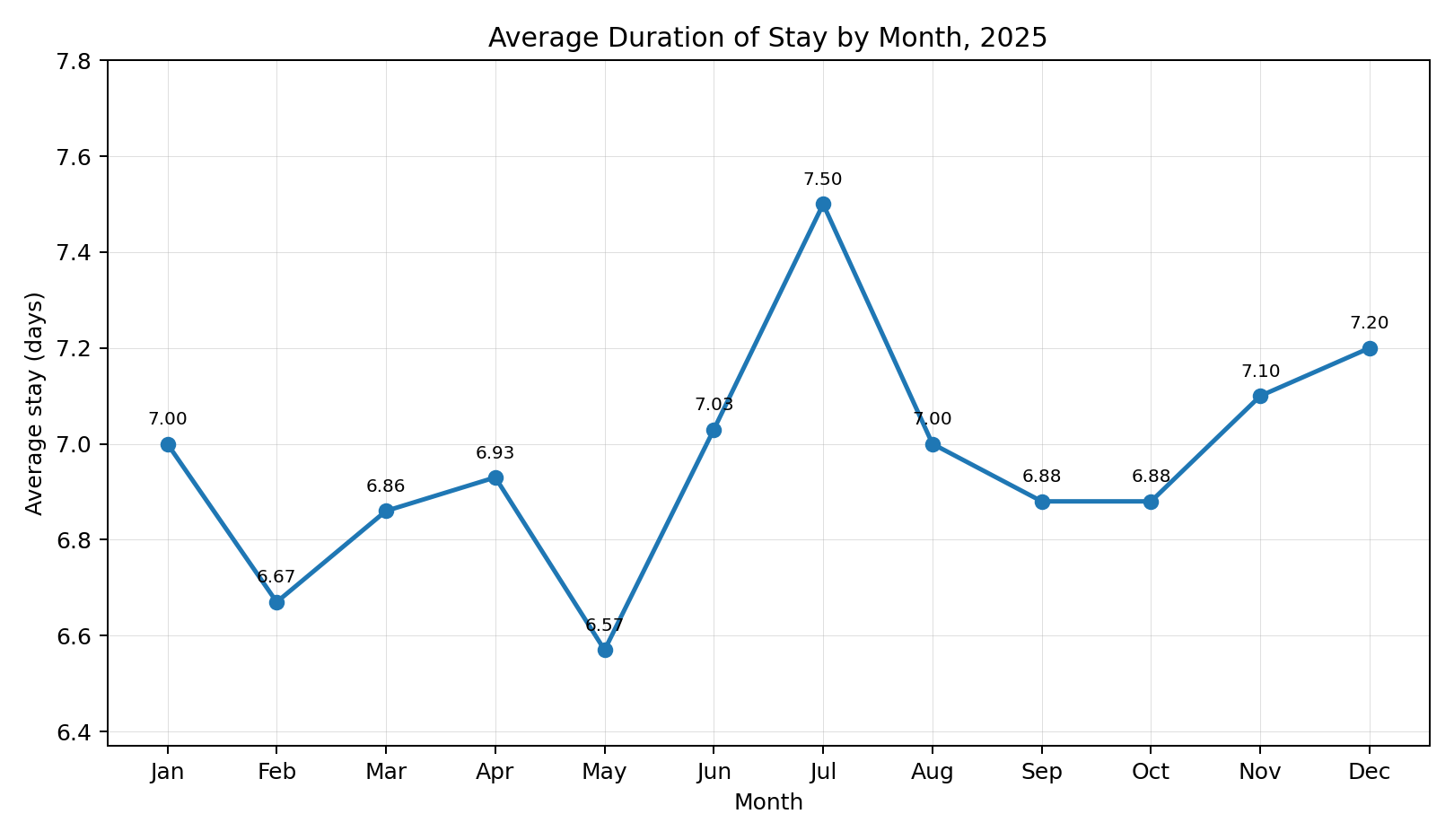

2025 was a seven-night market, but not evenly across the year

The monthly data for 2025 shows a relatively tight stay pattern. The lowest month was May, at 6.57 days. The highest month was July, at 7.50 days. The full monthly range was only 0.93 days, which is narrower than several earlier years in the dataset.

This tells me that the Maldives is no longer dealing with extremely volatile stay lengths across the year. Instead, it is operating around a fairly stable one-week model. That has practical value. Hotels, guesthouses, airlines, transfer operators, and destination marketers can design products around a predictable stay pattern.

However, the monthly details are important. July stands out at 7.50 days, followed by December at 7.20 days and November at 7.10 days. May was the weakest month, at 6.57 days. This suggests that the industry should not treat all months the same. A one-week average is useful, but there are still seasonal differences in how tourists use the destination.

For operators, the July figure is especially interesting. July is not usually discussed in the same way as the traditional high season, but the data shows that tourists who came in July 2025 stayed longer than tourists in any other month of that year. That creates an opportunity for summer family packages, diving products, local island experiences, wellness retreats, and longer-stay offers.

The 2025 decline was concentrated in the first half of the year

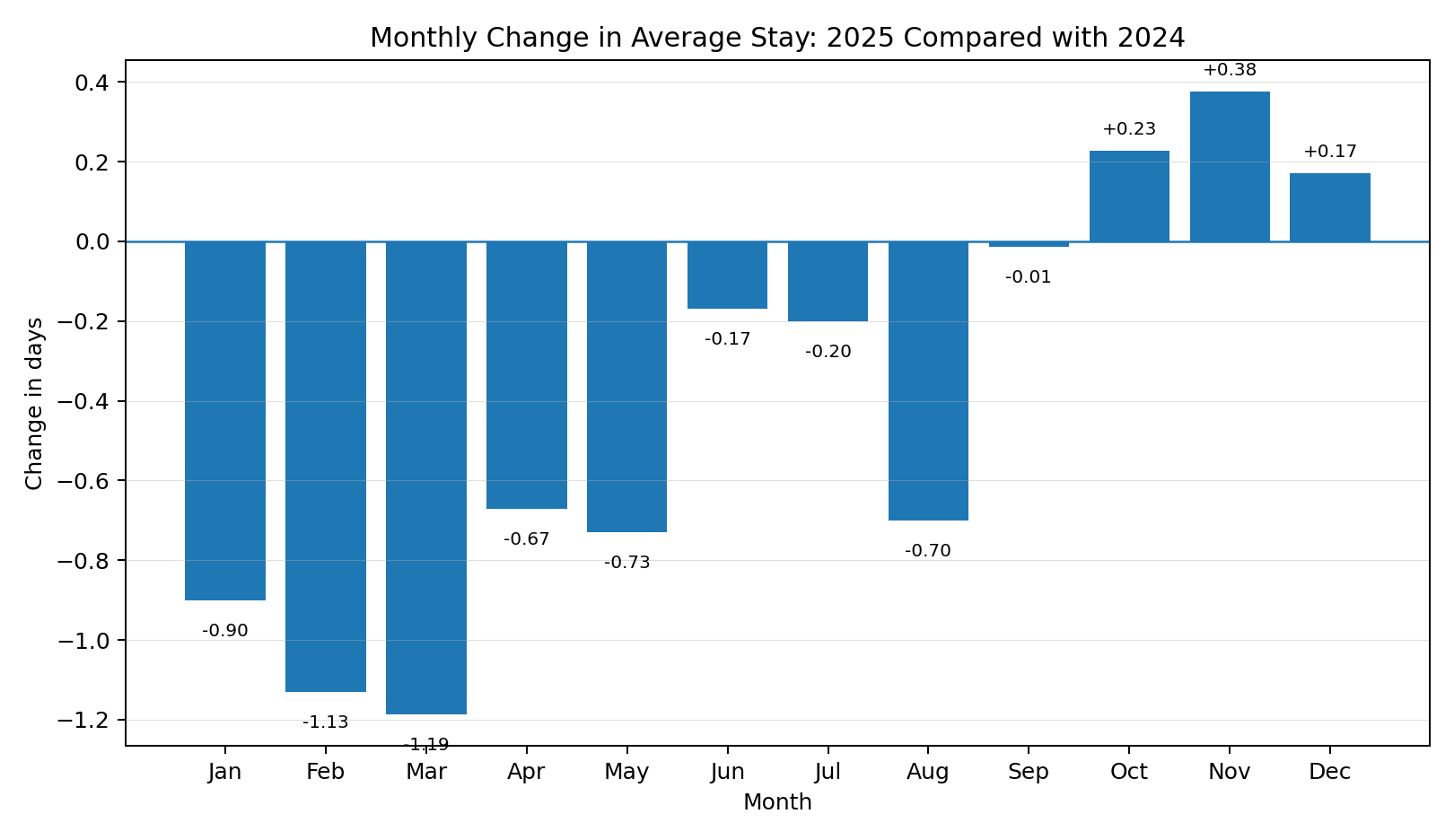

The comparison with 2024 reveals where the decline happened. In 2025, average stay was lower than 2024 in most months from January to September. The largest drops were in the first quarter: January fell by 0.90 days, February by 1.13 days, and March by 1.19 days. April and May also declined by around 0.67 to 0.73 days.

The pattern changed in the final quarter. October, November, and December 2025 were all slightly higher than the corresponding months in 2024. This matters because it suggests that the annual decline was not evenly distributed. The weakness was concentrated mainly in the first half of the year, while the last quarter showed signs of stabilisation or recovery.

For destination marketers, this is actionable. The first half of the year may need stronger product design to defend length of stay. The last quarter may already be more resilient. Marketing should not only aim to increase arrivals; it should aim to increase the number of nights attached to each arrival.

What the data reveals

The most valuable story from the dataset is that the Maldives is not simply returning to its pre-pandemic tourism model. It is entering a new stay-length equilibrium. The market is no longer as short-stay as the mid-2010s, but it is also no longer enjoying the long-stay conditions of the pandemic recovery period.

Practical implications for the tourism industry

For policymakers, the main implication is that arrivals should not be the only performance metric. Average stay directly affects tourism value. A small reduction in average stay can reduce visitor-days even when arrivals rise. This affects bed-night demand, tax collections, airport pressure, waste generation, and the efficiency of tourism infrastructure.

For destination marketers, the data suggests that the Maldives should market not only as a place to visit, but as a place to stay longer. A seven-night destination can become an eight-night destination if product design is right. This requires bundled experiences: reef excursions, wellness, cultural visits, diving, food experiences, island-hopping, family activities, and remote-work-friendly packages.

For resorts, the message is to protect length of stay through itinerary design. The room alone may not be enough. Guests need reasons to extend by one or two nights. This may come from multi-day wellness programmes, marine education, private dining, conservation activities, or packages linked to flights and transfers.

For guesthouses, the opportunity is different. Local-island tourism can increase stay length by offering more structured experiences: sandbank trips, diving, fishing, local food, island history, community-led tours, and multi-island circuits. But this requires better island-level coordination because the guesthouse product depends heavily on shared public goods.

For investors, the data suggests caution. If average stay is stabilising around seven days, investment models should not assume pandemic-era long-stay behaviour. Revenue projections should test sensitivity to average stay. A property that looks viable at 8.5 days may look different at 7.0 days.

Actionable recommendations

First, the Maldives should adopt average stay as a core tourism performance indicator alongside arrivals, bed nights, occupancy, and revenue per visitor. Monthly reporting should highlight whether growth is coming from more visitors or more nights. Second, destination marketing should target stay extension. Campaigns should not only ask tourists to choose the Maldives; they should give them reasons to add one more night. The most realistic goal is not to return to the 1980s average stay, but to move from around seven nights towards seven-and-a-half or eight nights in selected segments. Third, the industry should design seasonal stay-length strategies. The data shows that July 2025 had the highest average stay. This should be studied further. If July attracts longer-stay visitors, the industry should identify which markets, accommodation types, and trip purposes are driving that pattern. Fourth, policymakers should connect stay length with value capture. A tourist who stays longer may generate more tax, employment, local spending, and environmental pressure. The government should therefore analyse stay length together with expenditure, accommodation type, source market, and environmental cost. Fifth, guesthouse islands should build local experience calendars. If tourists on local islands have more organised activities, they may stay longer. But this requires coordination among councils, guesthouses, excursion providers, cafés, waste managers, and transport operators.

Turning Stay-Length Data into Tourism Strategy

The 2025 data tells me that the Maldives has entered a more disciplined phase of tourism recovery. The industry can no longer rely on the unusually long stays created by pandemic-era travel conditions. Average stay has moved down from the 2021 peak, and by 2025 the market was operating close to a seven-night structure.

But the story is not negative. The 2025 average stay remains higher than in 2019. That means the Maldives has retained part of the recovery-era gain. The strategic task is now to defend and deepen that gain.

For the next phase of Maldives tourism, the question should not only be “How many tourists arrived?” It should be “How many nights did they stay, what value did those nights create, and what can be done to make each visit more productive for the destination?”

That is why average duration of stay deserves more attention. It is a bridge between arrivals and value. It helps policymakers understand tourism productivity. It helps operators design better packages. It helps investors make more realistic assumptions. And it helps destination marketers move from volume promotion to value-based tourism strategy.

The Maldives does not need to chase longer stays blindly. It needs to understand which visitors can stay longer, in which months, in which accommodation segments, and for what reasons. That is where the next layer of tourism intelligence should begin.