The Record Arrivals Paradox: Why 2025 Was Not Simply a Tourism Boom Year for the Maldives

26 May 2026, 14:06 · by izuhuree

When I first looked at the 2025 tourism numbers, the headline was easy to see: the Maldives had reached its highest-ever tourist arrivals. In that sense, 2025 was clearly a record year. But the more I examined the dataset, the less comfortable I became with describing it simply as a tourism boom. The question I ask is simple: Did the post-pandemic recovery of Maldives tourism produce a more efficient tourism economy, or was growth mainly driven by expanding accommodation capacity?

I argue in this blog that the Maldives’ 2025 tourism record should be celebrated, but not understood through arrivals alone. The country welcomed more tourists than ever before, confirming a strong post-pandemic recovery. However, the data also shows a more complex picture: bed nights increased, but operating bed capacity expanded even faster; guesthouses continued to grow as a major segment; Europe returned strongly as a source market; and Asia remained below its earlier share.

This creates what I call the record arrivals paradox. Maldives tourism has recovered in volume, but recovery is not the same as higher productivity. A tourism economy can grow by attracting more visitors, by generating more value from each visitor, or by expanding capacity across more operators. These forms of growth have different implications for utilisation, profitability, infrastructure pressure, environmental management, and long-term competitiveness.

The main finding is that 2025 should mark a shift in how Maldives tourism performance is measured. The next stage of analysis should move beyond arrivals forecasting towards tourism productivity and value capture. This means paying closer attention to bed nights, utilisation, capacity growth, source-market dependence, guesthouse governance, and the revenue, employment, tax, local linkage, and environmental finance generated per visitor and per bed.

The Headline: A Record Year for Arrivals

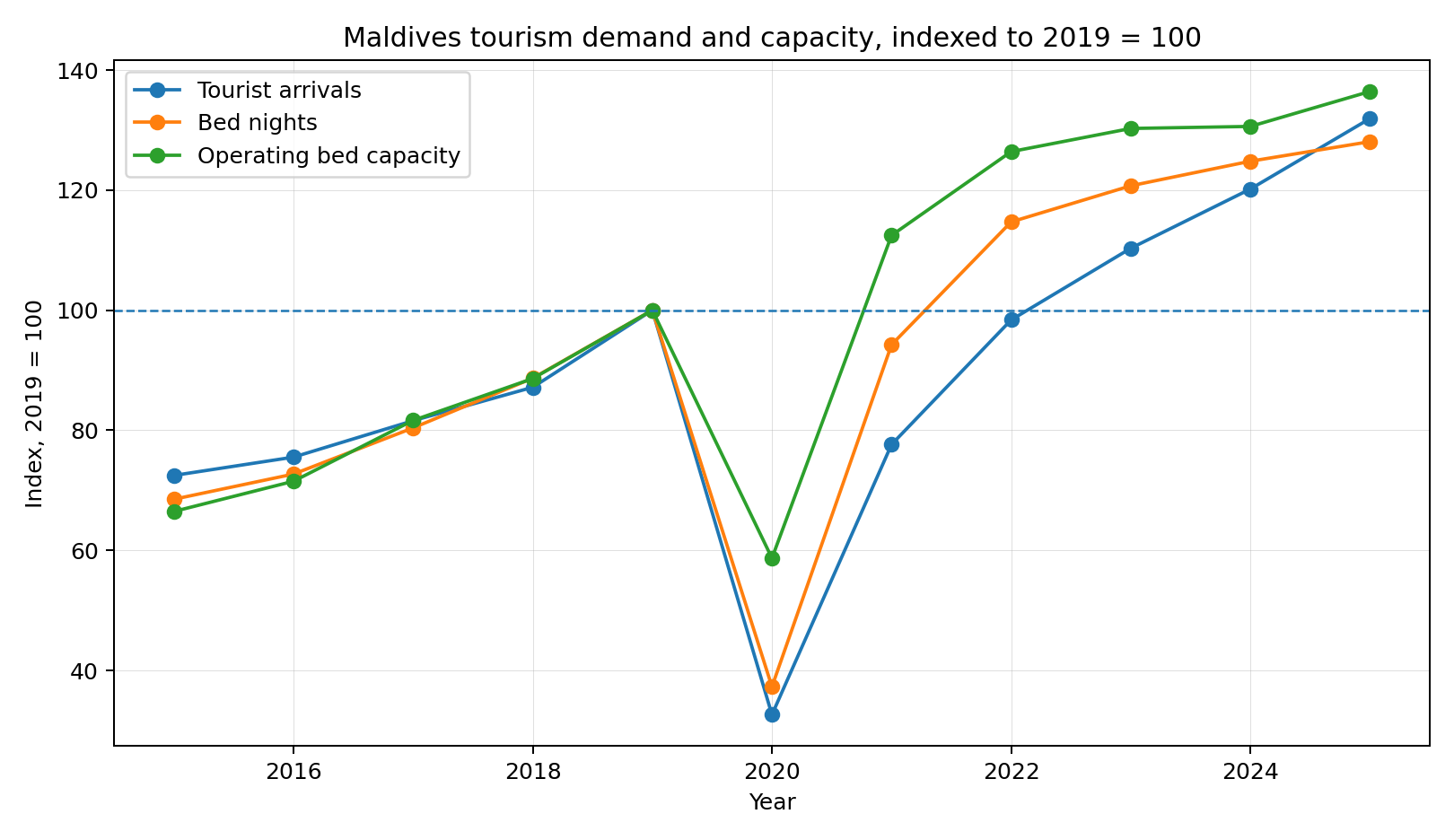

In 2025, the Maldives recorded 2,246,516 tourist arrivals. Compared with 1,702,887 arrivals in 2019, the last full pre-pandemic year, this represents an increase of about 31.9%.

That is a strong recovery by any standard. The Maldives did not merely return to its pre-pandemic level. It moved beyond it. For a tourism-dependent economy, this is significant. It means global demand for the Maldives remained resilient despite the disruption of the pandemic, changes in air connectivity, shifts in source markets, and wider uncertainty in the global economy.

But I do not think the arrivals figure alone gives us enough information. Tourism is not consumed as a single act of arrival. It is consumed through nights stayed, rooms occupied, transfers taken, meals purchased, activities booked, taxes paid, wages earned, and environmental resources used. For that reason, I treat arrivals as the starting point of the analysis, not the conclusion.

The Paradox: Capacity Expanded Faster Than Demand

The strongest finding in the dataset is that supply expanded faster than demand.

Between 2019 and 2025, tourist arrivals increased by 31.9%. Bed nights increased from 10.69 million to 13.69 million, or about 28.1%. But total operating bed capacity increased from 47,269 beds to 64,491 beds, or about 36.4%.

This is the core of the record arrivals paradox. The country had more tourists and more bed nights, but it also had a much larger accommodation base to fill. When capacity grows faster than bed-night demand, the industry can record higher arrivals while still experiencing softer utilisation.

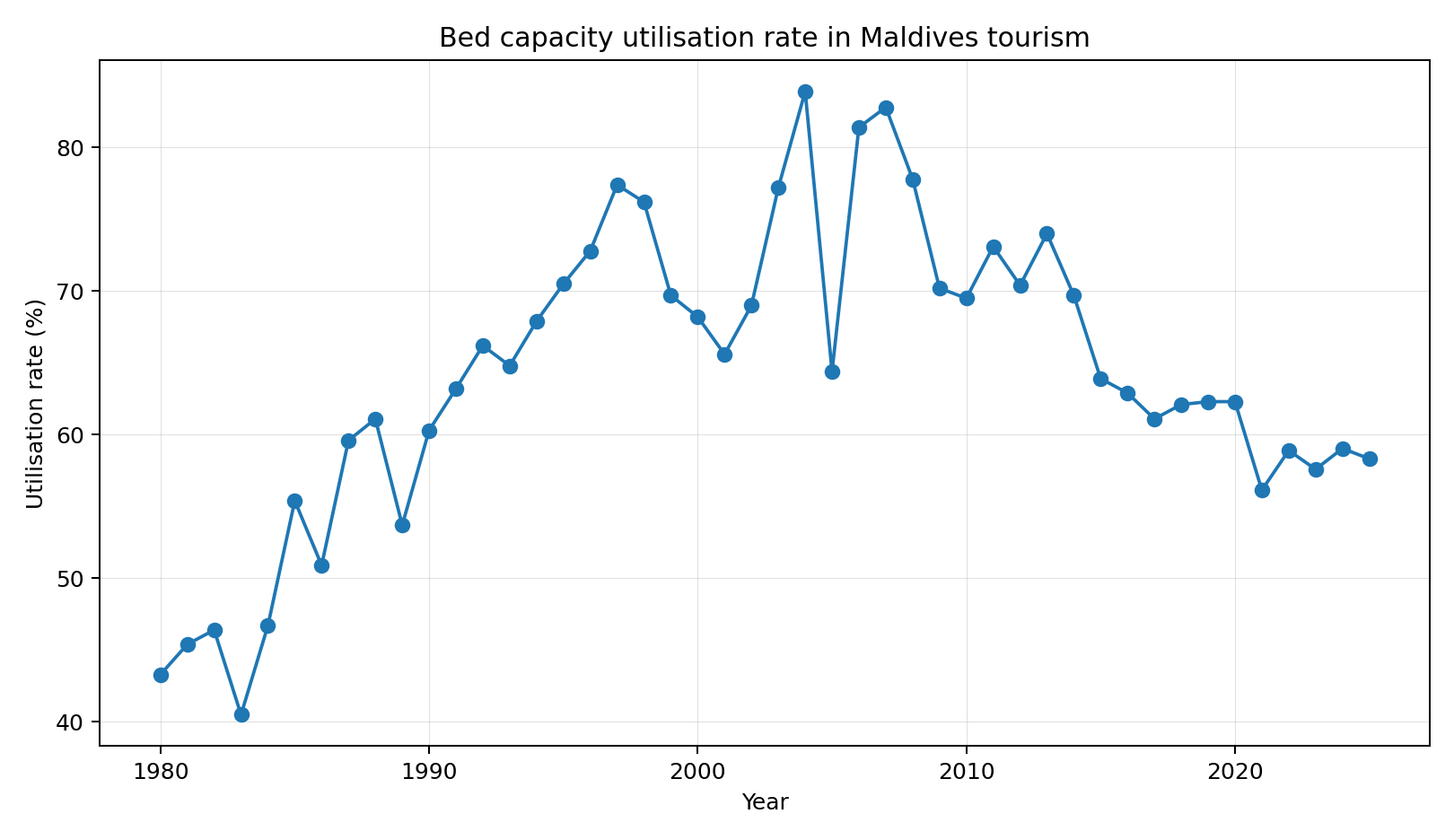

This is exactly what the utilisation data shows. In 2019, bed capacity utilisation stood at 62.3%. In 2025, it was 58.32%. That does not mean 2025 was weak. It means that the record arrivals year did not fully absorb the enlarged supply base.

For policymakers, this distinction matters. If the national conversation focuses only on arrivals, the policy response will be to attract even more tourists. But if the conversation includes utilisation, bed nights, capacity, and value capture, the policy question changes. It becomes: Are we using the tourism capacity we have already built efficiently enough?

Bed Nights Tell a Deeper Story Than Arrivals

I pay close attention to bed nights because they are closer to actual tourism consumption than arrivals. A visitor who stays three nights and a visitor who stays ten nights both count as one arrival, but they have very different economic implications.

In 2025, bed nights reached 13.69 million, compared with 10.69 million in 2019. This is a major increase. But the rate of growth in bed nights remained below the rate of growth in operating capacity.

Average stay also changed. In 2019, the average stay was 6.3 nights. In 2025, it was 7.0 nights. This is higher than before the pandemic, but lower than the unusually long stays seen during the early recovery period. In 2021, for example, average stay reached 8.8 nights, reflecting the unusual travel conditions of the pandemic period.

By 2025, the market appears to have normalised. Tourists were still staying slightly longer than in 2019, but the exceptional long-stay effect had faded. This matters because the Maldives cannot rely only on more arrivals. It also needs to understand length of stay, visitor spending, accommodation type, and source-market behaviour.

The Guesthouse Segment Is No Longer Marginal

The second major pattern I see is the continued structural rise of guesthouses.

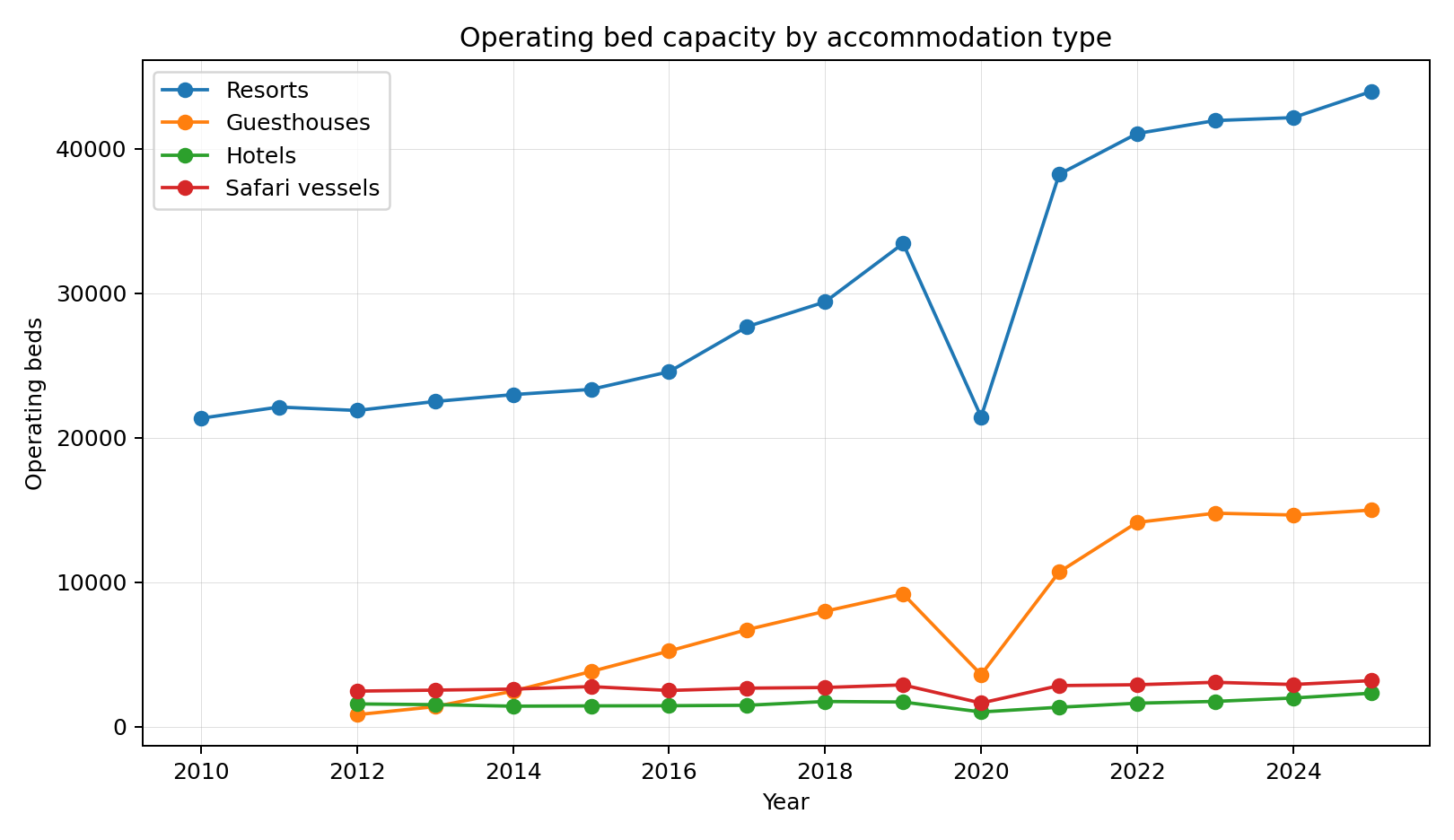

In 2019, the Maldives had 561 operational guesthouses. By 2025, this had increased to 876. Guesthouse operating bed capacity rose from 9,200 beds in 2019 to 14,999 beds in 2025. That is an increase of about 63.0%.

This is not a small side story. Guesthouses accounted for about 19.5% of total operating bed capacity in 2019. By 2025, their share had risen to about 23.3%.

This change is important because guesthouse tourism alters the geography and political economy of Maldives tourism. Resorts remain dominant, especially in terms of value, brand positioning, and high-end accommodation. But guesthouses bring tourism into inhabited islands. They connect tourism more directly with local councils, local businesses, households, cafés, shops, excursions, harbours, waste systems, and public beaches.

This creates opportunities for wider local participation. It also creates new management problems. In the one-resort-one-island model, many tourism costs are internalised within the resort island. In the guesthouse model, tourists use shared local island resources. Beaches, roads, harbours, waste areas, reefs, and public spaces become part of the tourism product, but no single operator fully controls or pays for them.

This is why the expansion of guesthouses should not be analysed only as an accommodation trend. It is also an infrastructure, environmental, governance, and local development issue.

Utilisation Is the Warning Signal

The utilisation rate is one of the most important indicators in the dataset because it tells us whether the industry is converting capacity into actual use.

In 2025, utilisation was below the 2019 level. This is significant because the public narrative around tourism often celebrates record arrivals without asking how efficiently accommodation capacity is being used.

A useful derived indicator is bed nights per operating bed. In 2019, the Maldives generated about 226 bed nights per operating bed. In 2025, it generated about 212 bed nights per operating bed. This suggests that each operating bed produced fewer annual bed nights than before the pandemic, even though total arrivals were higher.

I do not read this as a crisis. I read it as a productivity signal. It tells us that the next phase of Maldives tourism should pay more attention to yield, occupancy, market mix, pricing, environmental cost, and value per visitor.

A country can keep adding rooms and beds, but if demand does not keep pace, competition intensifies. Some operators may reduce prices. Others may depend more heavily on online travel agencies or short-term promotions. Public infrastructure may face more pressure, while private returns become more uneven. This is why capacity planning should be treated as a strategic issue, not only a licensing or investment issue.

Europe Returned Strongly, But Asia Remained Below its Earlier Share

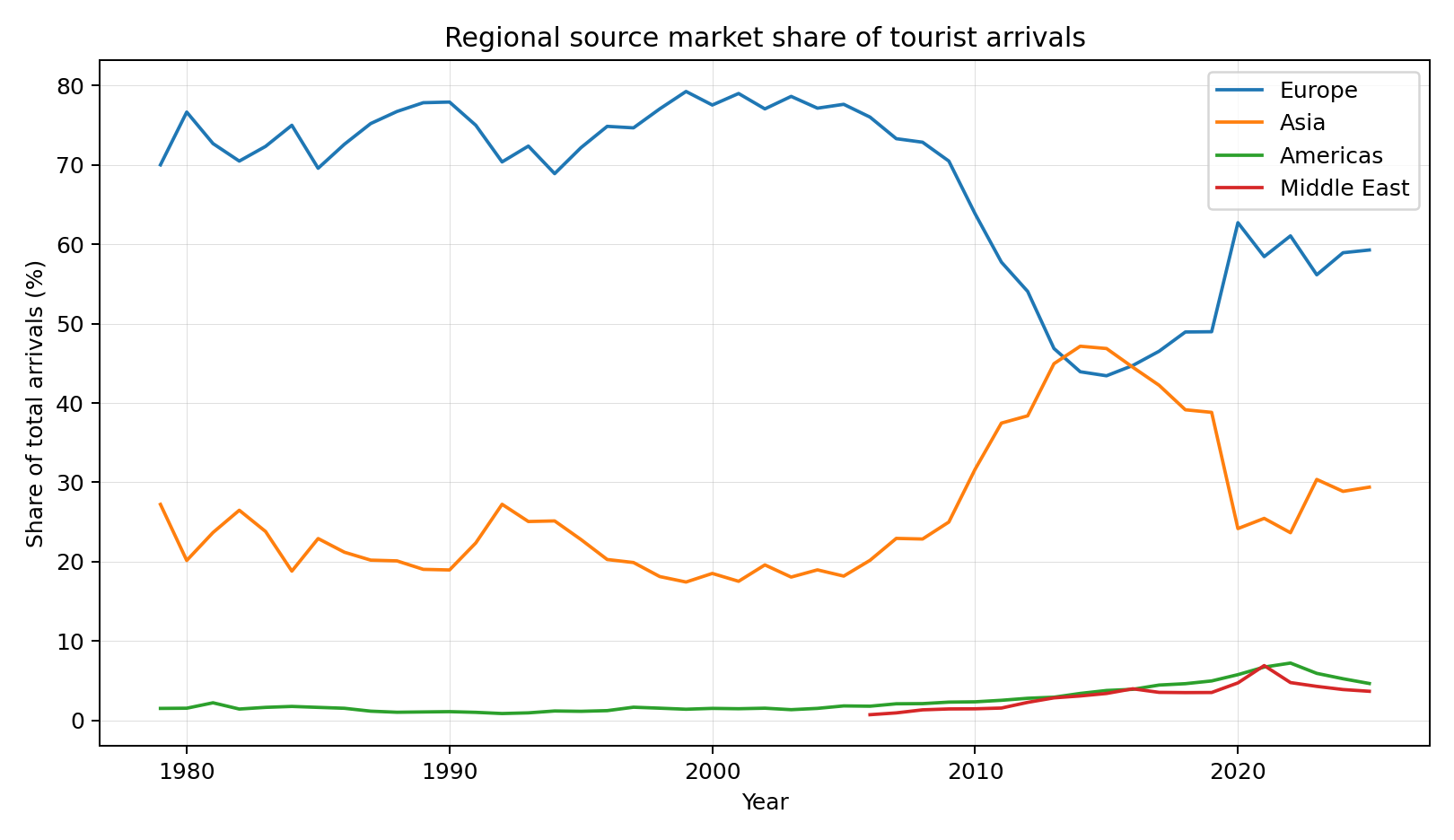

The source-market data also shows an important shift. In 2019, Europe accounted for about 49.0% of tourist arrivals, while Asia accounted for about 38.8%. By 2025, Europe’s share had risen to about 59.3%, while Asia’s share had fallen to about 29.4%.

This tells me that the post-pandemic recovery was not evenly distributed across regions. Europe returned strongly and became even more central to the Maldives tourism market. Asia, while still highly important, had not returned to its earlier share in the overall market by 2025.

This has several implications. European markets may support longer stays and higher-value segments in some parts of the industry. But a higher dependence on one region also creates vulnerability. If Europe faces recession, currency weakness, aviation disruption, or changes in travel preferences, the Maldives could be exposed.

For that reason, I would not only track total arrivals by source market. I would also track source-market performance by average stay, spending, accommodation type, seasonality, repeat visitation, transfer mode, and environmental preferences. A market that brings fewer tourists but longer stays and higher spending may be more valuable than a market that brings larger numbers but lower yield.

Why 2025 Should Change the Tourism Conversation

The main lesson I take from 2025 is that the Maldives needs a richer way of measuring tourism success.

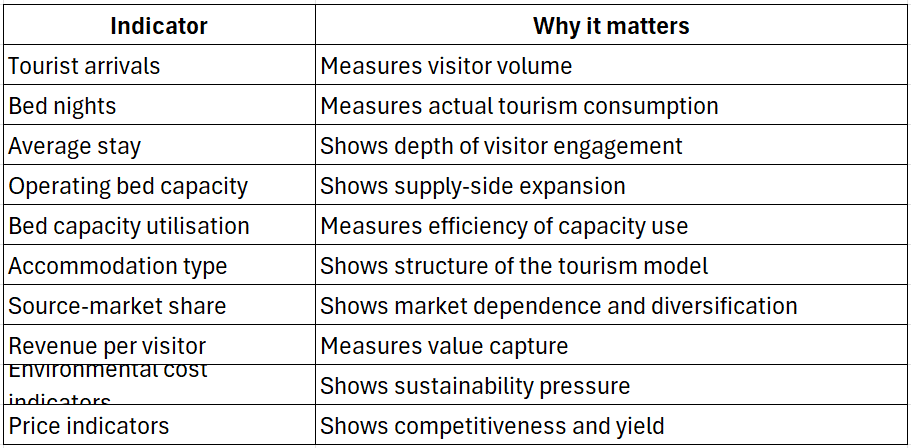

Arrivals are politically and publicly powerful because they are easy to understand. But they are not enough. A serious tourism performance framework should include at least the following indicators:

This is where more quantitative research can add value. It can move the public conversation from “How many tourists arrived?” to “What kind of tourism growth are we producing?”

That distinction is essential. More tourists do not automatically mean better tourism. More beds do not automatically mean more value. More guesthouses do not automatically mean more inclusive development unless local linkages, infrastructure, waste management, and environmental protection are also strengthened.

What the Data Suggests for Policy

I draw five policy implications from this analysis.

First, the Maldives should treat bed capacity expansion as a strategic variable. More capacity can support growth, but uncontrolled or poorly coordinated expansion may reduce utilisation and weaken returns. Second, the guesthouse segment requires island-level management systems. This includes waste, beach management, reef protection, zoning, visitor facilities, safety standards, and local infrastructure. Third, tourism performance should be measured through bed nights and utilisation, not arrivals alone. These indicators give a better picture of whether the industry is using its capacity efficiently. Fourth, market diversification should remain a priority. Europe’s strong return is positive, but excessive dependence on any one region creates risk. Fifth, the next phase of tourism policy should focus on value capture. The Maldives should ask how much revenue, employment, tax, local linkage, and environmental finance are generated per visitor and per bed.

From Recovery to Value: What the 2025 Record Really Shows

I would describe 2025 as a successful recovery year, but not simply as a boom year. The distinction matters.

The Maldives attracted more tourists than ever before. That confirms the strength of the destination brand and the resilience of the tourism economy. But the dataset also shows that the country is carrying a much larger accommodation base than it did before the pandemic. Capacity has grown faster than bed-night demand. Utilisation has not returned to the 2019 level. Guesthouses have become structurally important. Source-market composition has shifted.

So the real lesson of 2025 is not just that Maldives tourism has recovered. It is that the next stage of analysis must move from volume to value.

For me, this is the central purpose of more deeper analysis. It should not simply record that arrivals increased. It should explain what that increase means. It should help us see whether growth is efficient, inclusive, profitable, resilient, and environmentally sustainable.

The record arrivals paradox is therefore a useful warning and an opportunity. It warns us not to confuse more tourists with better tourism performance. But it also gives us an opportunity to build a stronger evidence base for the next phase of Maldives tourism policy.

The Maldives has recovered. The next question is whether it can turn that recovery into higher value, better utilisation, stronger local benefits, and more sustainable destination management.