The Hidden Geography of Maldives Tourism: Where is tourism really concentrated?

13 Jun 2026, 19:45 · by i.zuhuree

Maldives tourism has expanded across islands, but capacity and value remain concentrated. Resorts dominate beds and pricing, while guesthouse clusters urgently need spatial strategy, differentiation, and stronger destination management now.

When I look at the Maldives tourism data, I see a map.

Not a simple map of islands, but a map of economic weight: where beds are concentrated, where resorts dominate, where guesthouses cluster, where price signals value, and where future pressure will build. The Maldives is not one tourism economy. It is several tourism economies layered across the archipelago.

This seven-part series follows that hidden structure. And I try to answer the following questions: Where is tourism really concentrated?, Why do resorts still dominate beds and value? What did local-island tourism change? How have source markets reshaped risk? What do prices reveal about value capture? Where do reefs, waste, and crowding enter the economics? and What should the industry do next?

Today I begin with geography, because national averages can hide the most important fact: Maldives tourism has expanded, but it has not expanded evenly.

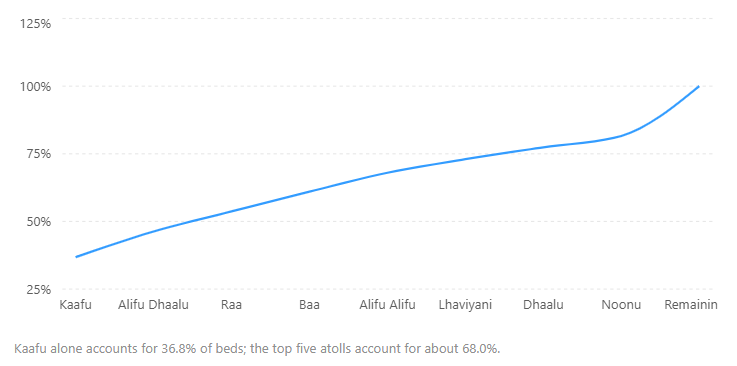

Cumulative concentration of tourism beds by atoll

Atolls ranked from largest to smallest bed capacity. The curve rises sharply because a few atolls carry most national tourism beds.

Kaafu, Alifu Dhaalu, Raa, Baa, and Alifu Alifu account for about 68.0%.

This is not random. Tourism follows access, airport proximity, resort island availability, transfer networks, investor confidence, and market history. Kaafu’s dominance reflects its role as the gateway atoll. Raa, Baa, Noonu, Lhaviyani, and Dhaalu reflect another pattern: resort-led expansion into high-value island zones.

The data therefore changes the question. Instead of asking whether Maldives tourism is growing, I want to ask: where is it growing, through which accommodation model, and at what value level?

The next figure shows why facility count alone is not enough.

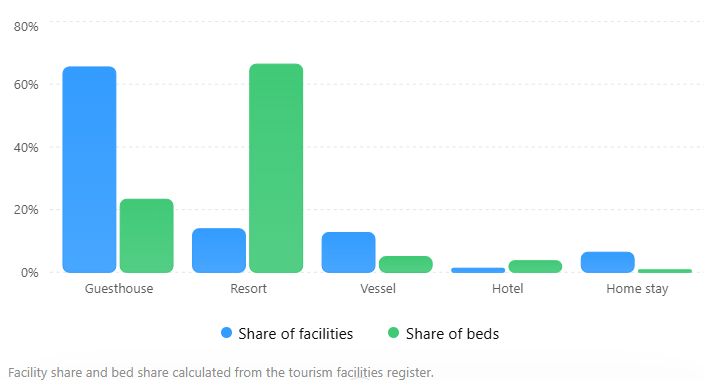

Accommodation model imbalance

Guesthouses dominate facility count, but resorts dominate bed capacity.

For some this data is a major surprise. Guesthouses account for 65.5% of all facilities, but only 23.3% of beds. Resorts are only 13.9% of facilities, but hold 66.4% of beds.

So the Maldives has broadened participation without replacing the resort-led capacity structure. Guesthouses changed who could enter tourism: small investors, island entrepreneurs, family businesses, and local communities. But resorts still carry most of the country’s physical accommodation weight.

For policymakers, this distinction matters. Facility count tells us about participation. Bed capacity tells us about scale. Price tells us about value. We need all three.

The atoll-level picture becomes even more useful when we classify places by their accommodation model.

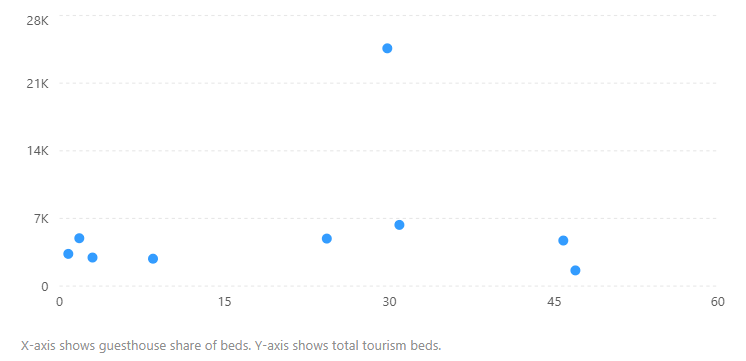

Atoll tourism model matrix

Atolls with low guesthouse share and high bed capacity are structurally resort-led; mixed atolls combine resort and guesthouse capacity.

The scatterplot turns the map into a policy tool. Lhaviyani, Dhaalu, Raa, and Noonu are structurally resort-led. Vaavu and Alifu Alifu are much more mixed. Kaafu is unusual: it is large, diverse, and still resort-led in capacity.

A resort-heavy atoll needs policies around lease management, high-value access, labour supply, environmental compliance, and premium positioning. A mixed atoll needs a different toolkit: public waste systems, beach zoning, harbour management, local-island branding, visitor behaviour rules, and guesthouse quality upgrading.

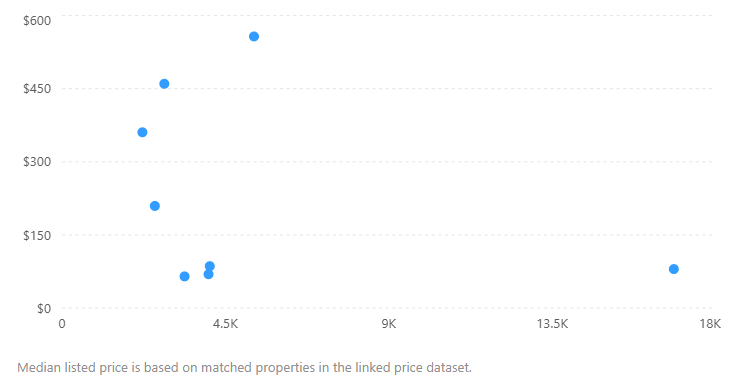

Atoll value positioning: beds versus listed price

Some atolls dominate through scale, while others show stronger resort-led price positioning.

Adding price makes the story sharper. Kaafu dominates scale, but not median price. Raa and Lhaviyani sit much higher on price because they are more resort-led. This matters because capacity and value are related, but not identical.

In the matched data, the median listed resort price is US$496, while the median listed guesthouse price is US$65. The resort median is about 7.6 times the guesthouse median. That does not mean every resort is profitable or every guesthouse is weak; listed prices are not actual revenue. But it does show market positioning.

The simple lesson is this: many beds do not automatically mean high value, and many facilities do not automatically mean strong value capture.

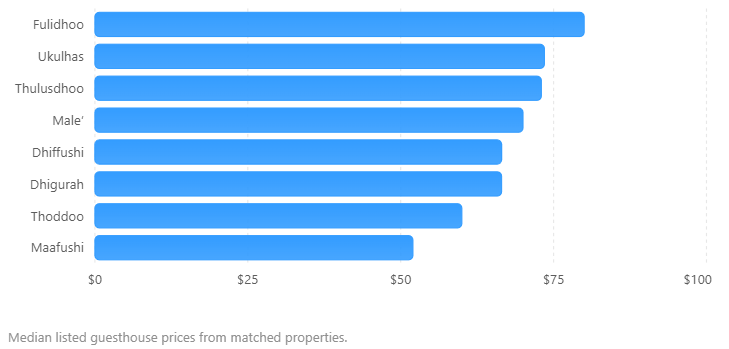

Guesthouse island pricing ladder

Major guesthouse islands occupy different price positions, suggesting different competitive strategies.

Maafushi has scale, but its median listed guesthouse price is relatively low at US$52. Fulidhoo, Ukulhas, and Thulusdhoo show stronger price positioning. Thoddoo and Dhigurah have strong review scores in the matched data, suggesting room for value upgrading if product design, activities, service quality, and marketing improve.

This is why guesthouse islands should not copy each other. A surfing island, diving island, family island, agriculture-linked island, premium local island, and short-stay transfer island cannot all sell the same generic “Maldives guesthouse” product. The more generic the product, the more likely the island falls into price competition.

What the Map Is Really Telling Us

The Maldives tourism story is often told as a national success story. It is that, but it is also a story of uneven geography.

Guesthouses have widened participation, but resorts still dominate capacity and value. Tourism has spread across many islands, but guesthouse beds are concentrated in a limited number of clusters. Some atolls are resort economies. Others are mixed tourism systems. Some islands have scale. Others have pricing power.

For policymakers, the implication is clear: tourism pressure is spatial. Waste, beach crowding, reef use, water demand, harbour congestion, and community pressure will concentrate where beds and visitors concentrate.

For investors, the lesson is equally clear: do not invest based only on national growth. Study island-level capacity, median prices, reviews, access, activities, and competitive density. For operators, adding rooms is not the same as creating value. Pricing power comes from service quality, environmental quality, review performance, activities, room type, design, food, and brand clarity.

The next stage of Maldives tourism strategy should be built around spatial intelligence: where tourism is concentrating, which model dominates, where value is captured, and where pressure is building.

The map is not background. It is the structure of the industry.

In the next blog, I will examine the resort backbone of this map. I will try to answer why a relatively small number of resort facilities still hold most of the country’s beds, pricing power, and value.