Two Maldives Tourism Markets: What Pricing Data Really Tells Us

18 Apr 2026, 13:21 · by izuhuree

A snapshot of 651 Maldives listings reveals two distinct tourism economies: a broad, affordable guesthouse network and a high-value resort market. The data shows that destination quality, service delivery and smart pricing strategies matter as much as product type for competitiveness.

The Maldives is not one pricing market

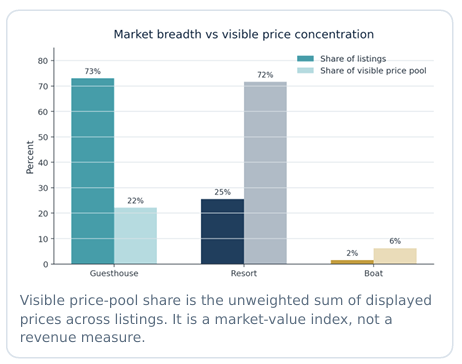

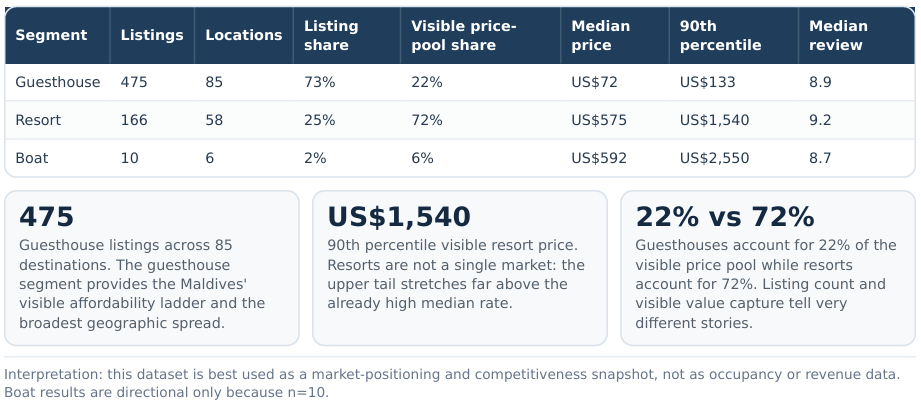

The strongest message from the brief is that the Maldives should not be read as a single tourism market. Instead, it operates through two different systems. On one side is a wide and geographically dispersed guesthouse market that carries affordability and local-island access. On the other is a resort market that captures most of the visible value online. In the dataset, guesthouses make up 475 listings across 85 destinations, or 73% of all listings, while resorts account for 166 listings across 58 destinations, or 25%. Yet resorts capture 72% of the visible price pool, compared with only 22% for guesthouses.

This gap becomes even clearer when price levels are compared. The median displayed rate for a resort is US575,whilethemedianforaguesthouseisonlyUS

72. The report therefore argues that national averages can be misleading. Averages flatten a market that is actually split between a broad-based value network and a concentrated premium economy. That distinction matters for investors, operators and policymakers alike.

Guesthouses are the backbone of affordability

The guesthouse segment is doing more than simply offering cheaper rooms. It provides the Maldives’ affordability ladder and its widest geographic reach. According to the brief, 78% of guesthouses in the sample are priced at US$100 or below. This means guesthouses are the main route through which a wider range of travellers can access Maldives tourism, and they are central to spreading tourism benefits beyond traditional resort zones.

What is especially important is that lower prices do not automatically mean lower value. The destination analysis shows that price is not the main determinant of perceived value in guesthouses. Several local-island destinations combine modest room rates with very strong guest reviews, outperforming some of the better-known gateway and volume markets.

Destination quality matters more than price alone

Some of the most compelling destinations in the guesthouse market are not the busiest or most obvious ones. The brief highlights six established local-island destinations that combine rates of US$80 or below with median review scores of 9.0 or higher: Dhangethi, Guraidhoo, Fuvahmulah, Huraa, Thoddoo and Ukulhas. These islands show that strong guest satisfaction can be delivered at relatively modest price points.

By contrast, some gateway and high-volume destinations appear to have management and service challenges. Male City and Hulhumale both record median guesthouse review scores of 7.5, well below the guesthouse segment median of 8.9. Maafushi, while affordable and high-volume, also sits below the stronger-performing islands on satisfaction. The implication is clear: in the guesthouse market, success depends less on room labels or convenience alone, and more on service quality, execution and overall destination management.

Resorts dominate premium capture through pricing strategy and product signals

The resort market tells a different story. Resorts are not just more expensive; they are also more active in revenue management. The brief finds that 53% of resorts show a markdown, with a median reduction of 35.1%, compared with 22% of guesthouses and a 24.6% median markdown. This suggests resorts are using pricing tactically to manage demand and protect competitiveness.

The commercial dynamics add another insight: free cancellation is not being priced as a premium feature. In both guesthouses and resorts, listings with free cancellation are actually cheaper than those without it. That means flexibility is functioning as a competitive lever, not as a luxury add-on.

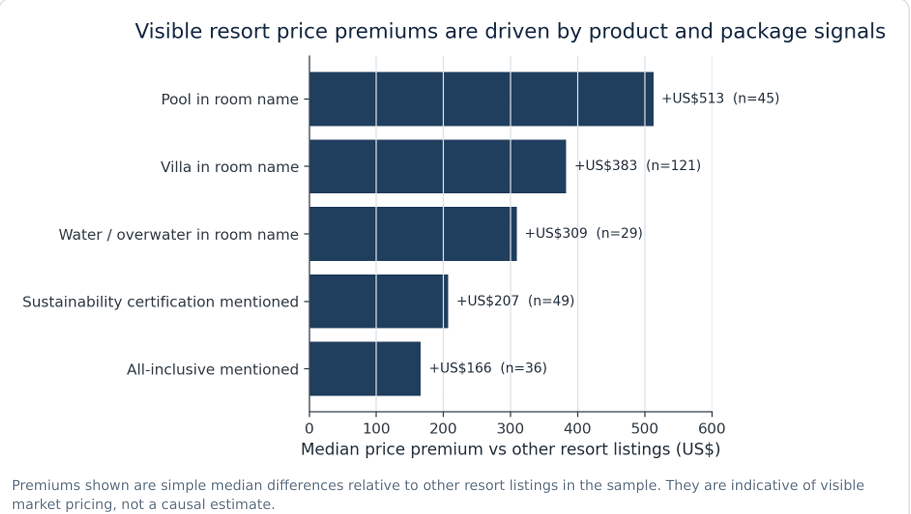

The same chart also shows what does support premium pricing in resorts. Product and package signals matter. Mentions of a pool in the room name, villa format, water or overwater positioning, all-inclusive packaging and sustainability certification are all associated with higher displayed prices. Meanwhile, sustainability remains concentrated in resorts, with 30% mentioning certification in listing text, compared with almost no visible presence in guesthouses.

What this means for the future

The policy and commercial lesson is straightforward. Managers should benchmark against the right destination and segment, not against national averages. A guesthouse in Thoddoo is not competing with a resort in North Malé Atoll. Policymakers, meanwhile, should protect the guesthouse affordability ladder, upgrade weaker gateway markets such as Male City, Hulhumale and Maafushi, and support local-island clusters that are already proving strong value.